Passenger traffic recovery continues in March 2022

- Like

- Digg

- Del

- Tumblr

- VKontakte

- Buffer

- Love This

- Odnoklassniki

- Meneame

- Blogger

- Amazon

- Yahoo Mail

- Gmail

- AOL

- Newsvine

- HackerNews

- Evernote

- MySpace

- Mail.ru

- Viadeo

- Line

- Comments

- Yummly

- SMS

- Viber

- Telegram

- Subscribe

- Skype

- Facebook Messenger

- Kakao

- LiveJournal

- Yammer

- Edgar

- Fintel

- Mix

- Instapaper

- Copy Link

Posted: 5 May 2022 | International Airport Review | No comments yet

The International Air Transport Association has released its passenger data for March 2022 showing that the recovery of air travel continues, with little impact from the conflict in Ukraine.

The International Air Transport Association (IATA) announced passenger data for March 2022 demonstrating that the recovery of air travel continues. Impacts from the conflict in Ukraine on air travel demand were quite limited overall while Omicron-related effects continued to be confined largely to Asian domestic markets.

Note: IATA have returned to year-on-year traffic comparisons, instead of comparisons with the 2019 period, unless otherwise noted. Owing to the low traffic base in 2021, some markets will show very high year-on-year growth rates, even if the size of these markets is still significantly smaller than they were in 2019.

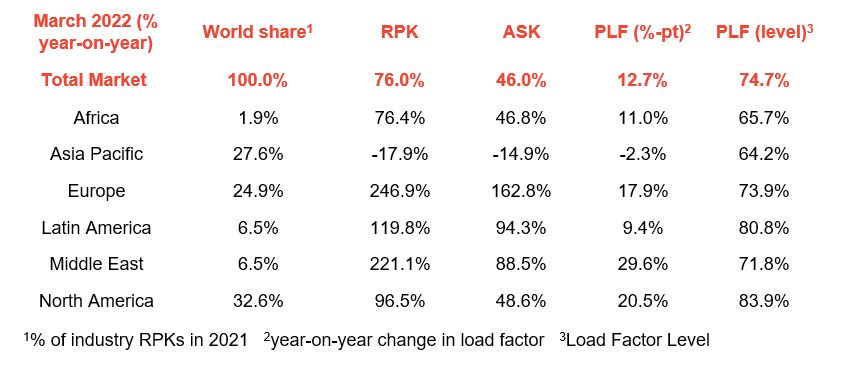

- Total traffic in March 2022 (measured in revenue passenger kms or RPKs) was up 76.0 per cent compared to March 2021. Although that was lower than the 115.9 per cent rise in February year-over-year demand, volumes in March were the closest to 2019 pre-pandemic levels, at 41 per cent below

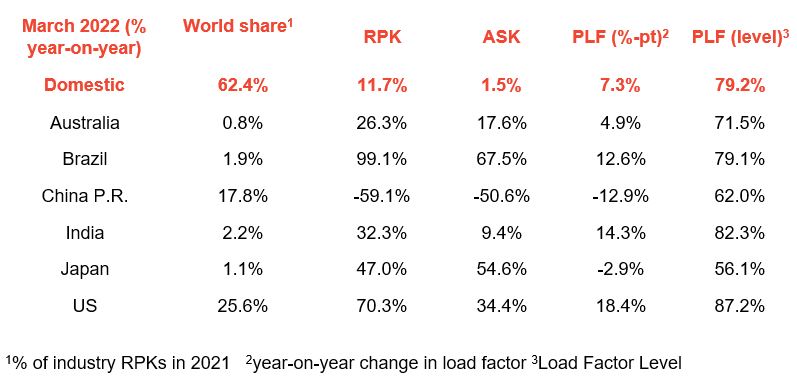

- March 2022 domestic traffic was up 11.7 per cent compared to the year-ago period, far below the 59.4 per cent year-over-year improvement recorded in February 2022. This largely was a result of the Omicron-related lockdowns in China. March domestic RPKs were down 23.2 per cent versus March 2019

- International RPKs rose 285.3 per cent versus March 2021, exceeding the 259.2 per cent gain experienced in February versus the year-earlier period. Most regions boosted their performance compared to the prior month, led by carriers in Europe. March 2022 international RPKs were down 51.9 per cent compared to the same month in 2019.

“With barriers to travel coming down in most places, we are seeing the long-expected surge in pent-up demand finally being realised. Unfortunately, we are also seeing long delays at many airports with insufficient resources to handle the growing numbers. This must be addressed urgently to avoid frustrating consumer enthusiasm for air travel,” commented Willie Walsh, IATA’s Director General.

Credit: IATA

International passenger markets

- European carriers continued to lead the recovery, with March traffic rising 425.4 per cent versus March 2021, improved over the 384.6 per cent increase in February 2022 compared to the same month in 2021. The impact of the war in Ukraine has been relatively limited outside of traffic to/from Russia and countries neighboring the conflict. Capacity rose 224.5 per cent, and load factor climbed 27.8 percentage points to 72.7 per cent

- Asia-Pacific airlines had a 197.1 per cent rise in March traffic compared to March 2021, up over the 146.5 per cent gain registered in February 2022 versus February 2021. While China and Japan remain restrictive to foreign visitors, other countries are becoming more relaxed, including South Korea, New Zealand, Singapore, and Thailand. Capacity rose 70.7 per cent and the load factor was up 24.1 percentage points to 56.6 per cent, the lowest among regions

- Middle Eastern airlines’ traffic rose 245.8 per cent in March compared to March 2021, an improvement compared to the 218.2 per cent increase in February 2022, versus the same month in 2021. March capacity rose 96.6 per cent versus the year-ago period, and load factor climbed 31.1 percentage points to 72.1 per cent

- North American carriers experienced a 227.8 per cent traffic rise in March versus the 2021 period, slightly down on the 237.3 per cent rise in February 2022 over February 2021. Capacity rose 91.9 per cent, and load factor climbed 31.2 percentage points to 75.4 per cent

- Latin American airlines’ March traffic rose 239.9 per cent compared to the same month in 2021, little changed from the 241.9 per cent increase in February 2022 compared to February 2021. The region benefitted from the end of bankruptcy procedures for some of the main carriers based there. March capacity rose 173.2 per cent and load factor increased 15.8 percentage points to 80.3 per cent, which was the highest load factor among the regions for the 18th consecutive month

Domestic passenger markets

Credit: IATA

- African airlines had a 91.8 per cent rise in March RPKs versus a year ago, improved compared to the 70.8 per cent year-over-year increase recorded in February 2022 compared to the same month in 2021. Air travel demand is challenged by low vaccination rates on the continent as well as impacts from rising inflation. March 2022 capacity was up 49.9 per cent and load factor climbed 14.1 percentage points to 64.5 per cent

- China’s domestic traffic was down 59.1 per cent in March, compared to March 2021, which was a large reversal compared to the 32.8 per cent year-over-year growth recorded in February. This was owing to the drastic lockdowns and travel restrictions following the spread of Omicron in the country

- India’s domestic RPKs rose 32.3 per cent year-on-year in March, strongly reversing the 2.4 per cent decline in February versus the prior year.

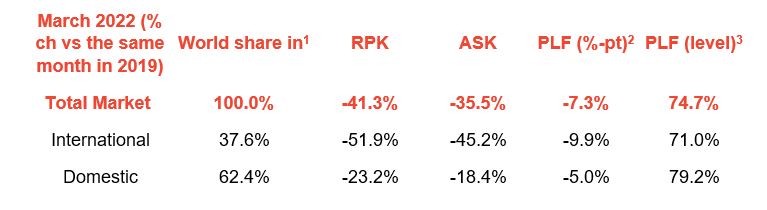

2022 vs 2019

March’s strong growth in most markers compared to a year ago, is helping passenger demand catch-up to 2019 levels. Total RPKs in March were down 41.3 per cent compared to March 2019, an improvement compared to the 45.5 per cent decline recorded in February versus the same month in 2019. The domestic recovery continues to outpace that of international markets despite the setback in China.

Credit: IATA

The Bottom line

“The ongoing recovery in air travel is excellent news for the global economy, for friends and families whose forced separations are being ended, and for the millions of people who depend on air transport for their livelihoods. Unfortunately, some government actions are emerging as key impediments to recovery. This is demonstrated most dramatically in the Netherlands.

“Schiphol airport is being allowed by the regulator to repay itself on the back of airlines and consumers for COVID-19 losses with a 37 per cent hike in airport charges over the next three years. Simultaneously, the airport has asked airlines to cancel bookings and new sales this week, at huge inconvenience to passengers, claiming shortfalls in airport staffing, including government provided security functions. And the government itself is planning to increase passenger taxes by €400 million annually with the stated purpose of discouraging travel.

“Seeing the Dutch government work to dismantle connectivity, fail to provide critical airport operational resources and enable price gouging by its hub airport is a destructive triple whammy. These actions will cost jobs. They will hurt consumers who already struggling with price inflation. And they will deplete resources that airlines need to achieve their Net Zero sustainability commitment. The Dutch government has forgotten a key lesson from the COVID-19 crisis which is that everyone’s quality of life suffers without efficient air connectivity. It must reverse course, and others must not follow their terrible example. To secure the recovery and its economic and social benefits, the immediate priority is for governments to have plans in place to meet expected demand this summer. Many people have waited two years for a summer holiday – it should not be ruined through lack of preparation,” added Walsh.

Related topics

Air traffic control/management (ATC/ATM), Airside operations, Capacity, COVID-19, Passenger experience and seamless travel, Passenger volumes, Sustainability, Terminal operations, Workforce

Chief Executive Officer

Chief Executive Officer CEO

CEO Chief Operating Officer

Chief Operating Officer Head of Operations, Safety and Emergency

Head of Operations, Safety and Emergency Chief Strategy Development Officer

Chief Strategy Development Officer Head of Operations

Head of Operations Airport General Manager

Airport General Manager CEO

CEO Chief Executive Officer

Chief Executive Officer