Air cargo up by 2.9 per cent in February 2022

- Like

- Digg

- Del

- Tumblr

- VKontakte

- Buffer

- Love This

- Odnoklassniki

- Meneame

- Blogger

- Amazon

- Yahoo Mail

- Gmail

- AOL

- Newsvine

- HackerNews

- Evernote

- MySpace

- Mail.ru

- Viadeo

- Line

- Comments

- Yummly

- SMS

- Viber

- Telegram

- Subscribe

- Skype

- Facebook Messenger

- Kakao

- LiveJournal

- Yammer

- Edgar

- Fintel

- Mix

- Instapaper

- Copy Link

Posted: 11 April 2022 | International Airport Review | No comments yet

According to the International Air Transport Association’s latest data for the global air cargo markets in February 2022, demand increased due to a general relaxation of COVID-19 travel-related factors.

The International Air Transport Association (IATA) released data for global air cargo markets showing that demand increased in February 2022, despite a challenging operating backdrop.

Several factors benefitted air cargo in February compared to January 2022. On the demand side, manufacturing activity ramped-up quickly after the early February Lunar New Year holiday. Capacity was positively influenced by the general and progressive relaxation of COVID-19 travel restrictions, reduced flight cancellations due to Omicron-related factors (outside of Asia), and fewer winter weather operational disruptions.

Note: We are returning to year-on-year traffic comparisons, instead of comparisons with the 2019 period, unless otherwise noted. Cargo demand is tracking above pre-COVID-19 levels, although capacity is still constrained.

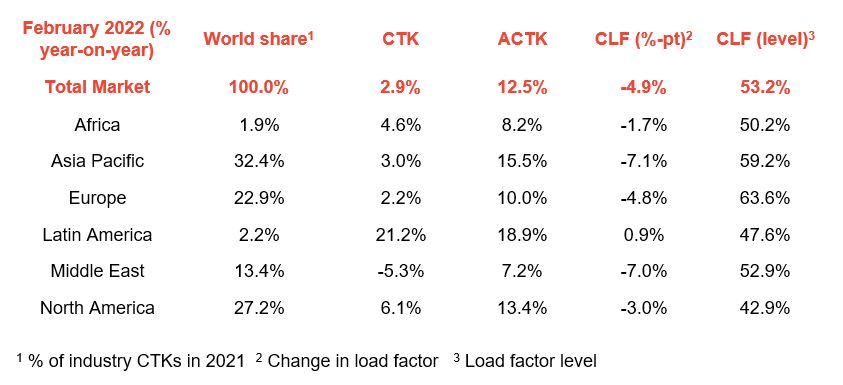

- Global demand, measured in cargo tonne-km (CTKs), was up 2.9 per cent compared to February 2021 (2.5 per cent for international operations)

- Adjusting the comparison for the impact of the Lunar New Year (which can cause volatility in reporting) by averaging January’s and February’s performance, demand increased 2.7 per cent year-on-year. While cargo volumes continued to rise, the growth rate decelerated from the 8.7 per cent year-on-year expansion in December

- Capacity was 12.5 per cent above February 2021 (8.9 per cent for international operations). While this is in positive territory, compared to pre-COVID-19 levels capacity remains constrained, 5.6 per cent below February 2019 levels

- Several factors in the operating environment should be noted:

- General consumer price inflation for the G7 countries was at 6.3 per cent year-on-year in February 2022, the highest since late 1982. While inflation normally curtails purchasing power this is balanced against higher savings levels coming out of the pandemic

- The Purchasing Managers’ Index (PMI) indicator tracking global new export orders fell to 48.2 in March 2022. This was the lowest since July 2020 indicating that a majority of surveyed businesses reported a fall in new export orders

- The zero-COVID policy in mainland China and Hong Kong continues to create supply chain disruptions as a result of flight cancellations due to labor shortages, and because many manufacturers cannot operate normally.

The impact of Russia’s invasion of Ukraine had limited effect globally on February’s performance as it occurred very near the end of the month. The negative impacts of war and related sanctions (particularly higher energy costs and reduced trade) will become more visible from March 2022.

“Demand for air cargo continued to expand despite growing challenges in the trading environment. That is not likely to be the case in March (2022) as the economic consequences of the war in Ukraine take hold. Sanction-related shifts in manufacturing and economic activity, rising oil prices and geopolitical uncertainty will take their toll on air cargo’s performance,” commented Willie Walsh, IATA’s Director General.

Credit: IATA

February regional performance

- Asia-Pacific airlines saw their air cargo volumes increase 3.0 per cent in February 2022 compared to the same month in 2021. Available capacity in the region was up 15.5 per cent compared to February 2021, however it remains heavily constrained compared to pre-COVID-19 levels, down 14.6 per cent compared to February 2019. The zero-COVID policy in mainland China and Hong Kong is impacting performance

- North American carriers posted a 6.1 per cent increase in cargo volumes in February 2022 compared to February 2021. The ramp up of manufacturing activity in China following the end of the Lunar New Year resulted in growth in the Asia–North America market, with seasonally adjusted volumes rising by 4.3 per cent in February. Capacity was up 13.4 per cent compared to February 2021

- European carriers saw a 2.2 per cent increase in cargo volumes in February 2022 compared to the same month in 2021. This was slower than the previous month (6.4 per cent), partially attributable to the war in Ukraine which started at the end of the month. Seasonally adjusted demand on the Asia-Europe route, one of the most affected by the conflict decreased by 2.0 per cent month on month. Capacity was up 10.0 per cent in February 2022 compared to February 2021, and down 11.1 per cent compared to pre-crisis levels (2019)

- Middle Eastern carriers experienced a 5.3 per cent year-on-year decrease in cargo volumes in February 2022. This was the weakest performance of all regions, which was owing to a deterioration in traffic on several key routes such as Middle East-Asia, and Middle East-North America. Looking forward, there are signs of improvement as data indicate that the region is likely to benefit from traffic being redirected to avoid flying over Russia. Capacity was up 7.2 per cent compared to February 2021

- Latin American carriers reported an increase of 21.2 per cent in cargo volumes in February 2022 compared to the 2021 period. This was the strongest performance of all regions. Some of the largest airlines in the region are benefitting from the end of bankruptcy procedures. Capacity in February was up 18.9 per cent compared to the same month in 2021

- African airlines saw cargo volumes increase by 4.6 per cent in February 2022 compared to February 2021. Capacity was 8.2 per cent above February 2021 levels.

Related topics

Air freight and cargo, Airside operations, Capacity, Cargo, COVID-19, Terminal operations

Chief Executive Officer

Chief Executive Officer CEO

CEO Chief Operating Officer

Chief Operating Officer Head of Operations, Safety and Emergency

Head of Operations, Safety and Emergency Chief Strategy Development Officer

Chief Strategy Development Officer Head of Operations

Head of Operations Airport General Manager

Airport General Manager CEO

CEO Chief Executive Officer

Chief Executive Officer