IATA reveals global air cargo data for October 2021

- Like

- Digg

- Del

- Tumblr

- VKontakte

- Buffer

- Love This

- Odnoklassniki

- Meneame

- Blogger

- Amazon

- Yahoo Mail

- Gmail

- AOL

- Newsvine

- HackerNews

- Evernote

- MySpace

- Mail.ru

- Viadeo

- Line

- Comments

- Yummly

- SMS

- Viber

- Telegram

- Subscribe

- Skype

- Facebook Messenger

- Kakao

- LiveJournal

- Yammer

- Edgar

- Fintel

- Mix

- Instapaper

- Copy Link

Posted: 2 December 2021 | International Airport Review | No comments yet

According to International Air Transport Association’s latest data, demand for global air cargo increased by 9.4 per cent during October 2021.

The International Air Transport Association (IATA) released October 2021 data for global air cargo markets showing that demand continued to be well above pre-COVID-19 levels and that the capacity constraints have eased slightly.

As comparisons between 2021 and 2020 monthly results are distorted by the extraordinary impact of COVID-19, unless otherwise noted, all comparisons below are to October 2019 which followed a normal demand pattern.

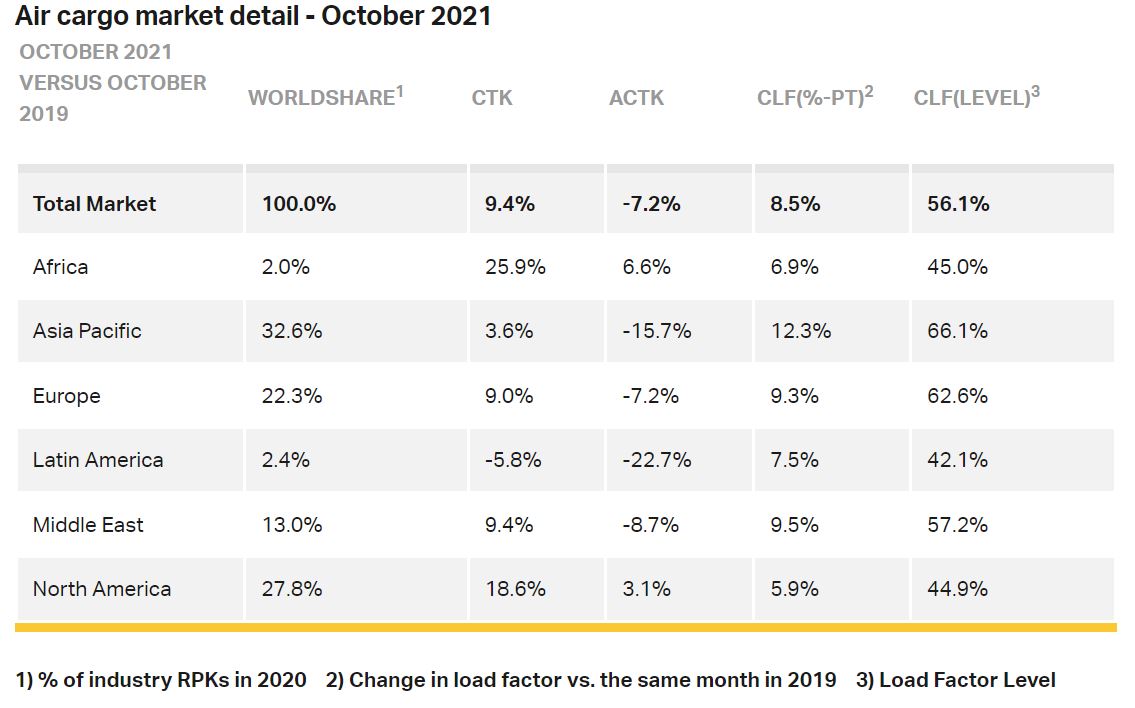

- Global demand, measured in cargo tonne-km (CTKs), was up 9.4 per cent compared to October 2019 (10.4 per cent for international operations)

- Capacity constraints have eased slightly but remain 7.2 per cent below pre-COVID-19 levels (October 2019) (-8.0 per cent for international operations).

Economic conditions continue to support air cargo growth but are slightly weaker than in the previous months. Several factors should be noted:

- Supply chain disruptions and the resulting delivery delays have led to long supplier delivery times. This typically results in manufacturers using air transport, which is quicker, to recover time lost during the production process. The global Supplier Delivery Time Purchasing Managers Index (PMI) reached an all-time low of 34.8 in October 2021; values below 50 are favourable for air cargo

- Relevant components of the October PMIs (new export orders and manufacturing output) have been in a gradual slowdown since May 2021 but remain in favourable territory

- The inventory-to-sales ratio remains low ahead of the peak year-end retail events such as Christmas. This is positive for air cargo as manufacturers turn to air cargo to rapidly meet demand

- Global goods trade and industrial production remain above pre-COVID-19 levels

- The cost-competitiveness of air cargo relative to that of container shipping remains favorable.

“October data reflected an overall positive outlook for air cargo. Supply chain congestion continued to push manufacturers towards the speed of air cargo,” said Willie Walsh, IATA’s Director General. “Demand was up 9.4 per cent in October compared to pre-COVID-19 levels. And capacity constraints were slowly resolving as more passenger travel meant more belly capacity for air cargo. The impact of government reactions to the Omicron variant is a concern. If it dampens travel demand, capacity issues will become more acute. After almost two years of COVID-19, governments have the experience and tools to make better data-driven decisions than the mostly knee-jerk reactions to restrict travel that we have seen to date. Restrictions will not stop the spread of Omicron. Along with urgently reversing these policy mistakes, the focus of governments should be squarely on ensuring the integrity of supply chains and increasing the distribution of vaccines.”

Credit: IATA

October Regional Performance

Asia-Pacific airlines saw their international air cargo volumes increase 7.9 per cent in October 2021 compared to the same month in 2019. This was close to a doubling in growth compared to the previous month’s four per cent expansion. The improvement was partly driven by increased capacity on Europe-Asia routes as several important passenger routes reopened. Belly capacity between the continents was down 28.3 per cent in October, much better than the 37.9 per cent fall in September. International capacity in the region eased slightly in October, down 12.9 per cent compared to the previous year, a significant improvement over the 18.9 per cent drop in September.

North American carriers posted an 18.8 per cent increase in international cargo volumes in October 2021 compared to October 2019. This was on par with September’s performance (18.9 per cent). Demand for faster shipping times and strong U.S. retail sales are underpinning the North American performance. International capacity was down 0.6 per cent compared to October 2019, a significant improvement from the previous month.

European carriers saw an 8.6 per cent increase in international cargo volumes in October 2021 compared to the same month in 2019, an improvement compared to the previous month (5.8 per cent). Manufacturing activity, orders and long supplier delivery times remain favourable to air cargo demand. International capacity was down 7.4 per cent compared to pre-COVID-19 levels, a significant improvement from the previous month, which was down 12.8 per cent on pre-crisis levels.

Middle Eastern carriers experienced a 9.4 per cent rise in international cargo volumes in October 2021 versus October 2019, a significant drop in performance compared to the previous month (18.4 per cent). This was due to a deterioration in traffic on several key routes such as Middle East-Asia, and Middle East-North America. International capacity was down 8.6 per cent compared to October 2019, a decrease compared to the previous month (four per cent).

Latin American carriers reported a decline of 6.6 per cent in international cargo volumes in October compared to the 2019 period, which was the weakest performance of all regions, but an improvement compared to the previous month (a 17 per cent fall). Capacity in October was down 28.3 per cent on pre-COVID-19 levels, a decrease from September, which was down 20.8 per cent on the same month in 2019.

African airlines saw international cargo volumes increase by 26.7 per cent in October, a deterioration from the previous month (35 per cent) but still the largest increase of all regions. International capacity was 9.4 per cent higher than pre-COVID-19 levels, the only region in positive territory, albeit on small volumes.

Related topics

Air freight and cargo, Airside operations, Capacity, COVID-19

Chief Executive Officer

Chief Executive Officer CEO

CEO Chief Operating Officer

Chief Operating Officer Head of Operations, Safety and Emergency

Head of Operations, Safety and Emergency Chief Strategy Development Officer

Chief Strategy Development Officer Head of Operations

Head of Operations Airport General Manager

Airport General Manager CEO

CEO Chief Executive Officer

Chief Executive Officer